Two of the most common assumptions about doing business in the UAE are now outdated and potentially costly. The first is that free zone companies are automatically tax-free. They are not. The second is that offshore companies have no UAE tax exposure. That is also not always true.

The introduction of UAE corporate tax in 2023 fundamentally changed how these structures are treated. What used to be a straightforward decision based on ownership, cost, and licensing has become a tax planning decision with long-term financial consequences.

Many businesses are still operating under structures that made sense before corporate tax was introduced but may no longer be optimal in 2026.

The reality is that mainland, free zone, and offshore entities are now treated very differently across corporate tax, VAT, and compliance requirements. The differences are not just technical. They directly affect how much tax you pay, what risks you carry, and how flexible your operations are.

This guide breaks down exactly how each structure works in 2026 and what you should be questioning about your current setup right now.

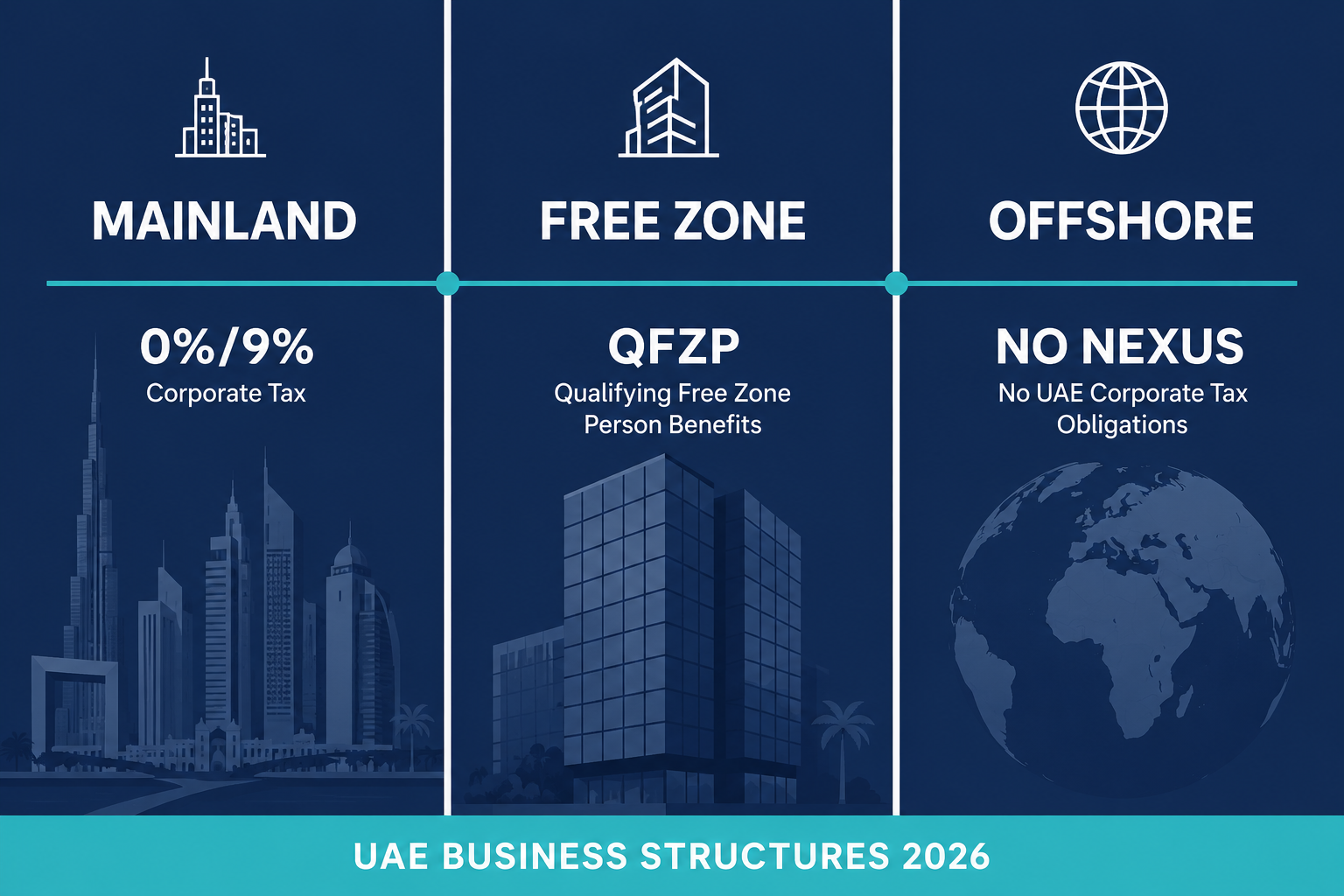

How Corporate Tax Applies to Each Structure

Mainland Companies

Mainland companies are licensed by UAE government authorities (such as the Department of Economic Development) and can operate freely across the UAE market without restrictions.

From a corporate tax perspective, the structure is straightforward:

- 0% tax on taxable income up to AED 375,000

- 9% tax on taxable income above AED 375,000

There is no distinction between qualifying and non-qualifying income. All taxable income is treated the same under this rate structure.

Mainland businesses may also benefit from Small Business Relief (SBR). If revenue does not exceed AED 3 million, the business can elect to treat its taxable income as zero for tax periods ending on or before 31 December 2026.

The key advantage of a mainland structure in 2026 is operational freedom. Mainland companies can transact with any customer across the UAE including individuals, corporates, or government entities without affecting their tax position.

Free Zone Companies

Free zone companies operate under a more complex corporate tax framework. They may qualify for a 0% corporate tax rate but only if they meet the criteria to be classified as a Qualifying Free Zone Person (QFZP). This status is not automatic and must be maintained continuously.

To qualify, all of the following conditions must be met:

- Adequate economic substance: The business must have real operations in the free zone, including employees, physical assets, and genuine activity.

- Qualifying income only: The 0% rate applies only to income from qualifying activities as defined by the Ministry of Finance.

- De minimis requirement: Non-qualifying income must not exceed 5% of total revenue or AED 5 million, whichever is lower.

- No mainland election: The business cannot elect to be treated as a mainland taxpayer.

- Arm’s length pricing: All related-party transactions must comply with transfer pricing rules.

If the de minimis threshold is exceeded or any of the conditions are not met, the consequences are significant:

- The company becomes subject to 9% corporate tax

- QFZP status is lost for five consecutive tax periods

It is also important to note that all free zone entities, whether qualifying or not, must:

- Register for corporate tax

- File annual returns with the FTA

Offshore Companies

Offshore companies (such as those incorporated in RAK ICC, JAFZA Offshore, or Ajman Offshore) are typically used for holding assets or conducting international business. Their corporate tax position depends on whether they have a UAE nexus.

- If the company has no UAE-sourced income and no permanent establishment in the UAE, it is generally outside the scope of UAE corporate tax.

- If the company generates UAE-sourced income or operates through a UAE permanent establishment, that income may be subject to corporate tax at standard rates.

This is the key distinction: offshore structures are not automatically tax-free. Their tax treatment depends entirely on the nature of their activities and where their income is generated.

A company holding international investments with no UAE operations may remain outside the corporate tax system. However, an offshore entity that effectively operates within the UAE market can fall within the tax net.

How VAT Applies to Each Structure

An important distinction many businesses miss: VAT operates independently of corporate tax. Your entity type, whether mainland, free zone, or offshore, does not automatically determine whether VAT applies. The key trigger is the AED 375,000 taxable supplies threshold, calculated over a rolling 12-month period.

Mainland Companies

For mainland businesses, VAT rules are straightforward. If taxable supplies exceed AED 375,000, VAT registration is mandatory. Once registered:

- Standard-rated supplies are taxed at 5%

- Certain supplies may be zero-rated or exempt, depending on their nature

There are no special VAT concessions tied to being a mainland entity. Compliance follows standard UAE VAT law.

Free Zone Companies

Free zone status does not exempt a business from VAT. If a free zone company crosses the AED 375,000 threshold, it must register and comply with all VAT obligations just like a mainland business.

The only exception relates to Designated Zones, which are specific free zones that are treated as outside the UAE for VAT on goods only, under certain conditions.

Even in these cases:

- The exception is narrow and highly conditional

- It applies mainly to the movement of goods within or between designated zones

- Services are not covered — services supplied from a free zone to mainland customers are generally subject to 5% VAT

Offshore Companies

Offshore companies are generally outside the UAE VAT system if they do not conduct business within the UAE. However, VAT obligations can arise if:

- The offshore company makes taxable supplies within the UAE

- The nature of the transaction triggers VAT under UAE rules

For example, supplying goods or services to UAE customers can create VAT exposure depending on the structure of the transaction.

Compliance Obligations by Structure

Corporate tax and VAT are only part of the picture. Each structure carries its own ongoing compliance obligations, which businesses must manage consistently.

Mainland Companies

Mainland businesses must:

- Register for corporate tax and file annual returns

- Register for VAT if above the threshold

- Maintain records for at least 7 years for corporate tax purposes

- Comply with transfer pricing rules for related-party transactions

- Prepare audited financial statements if revenue reaches AED 50 million or more

Free Zone Companies

Free zone entities face stricter ongoing requirements, especially if aiming to maintain QFZP status. They must:

- Register for corporate tax and file annual returns, regardless of whether taxed at 0% or 9%

- Maintain audited financial statements (mandatory for QFZP)

- Demonstrate economic substance annually

- Comply with transfer pricing rules

- Register for VAT if above the threshold

Offshore Companies

Compliance obligations for offshore entities depend on their level of UAE activity.

- If there is no UAE nexus, corporate tax registration may not be required

- If UAE-sourced income or a permanent establishment exists, registration and filing obligations apply

- Offshore companies are typically not VAT registered unless making taxable UAE supplies

- They must still maintain records in line with their registration authority (e.g., RAK ICC)

Structure Comparison at a Glance

| Factor | Mainland | Free Zone | Offshore |

|---|---|---|---|

| Corporate Tax Rate | 0% / 9% | 0% (if QFZP) / 9% | Depends on UAE nexus |

| QFZP Required | No | Yes, for 0% rate | Not applicable |

| VAT Threshold | AED 375,000 | AED 375,000 | If UAE supply made |

| Tax Filing Required | Yes | Yes (always) | Only if UAE nexus |

| Audited Financials | AED 50M+ revenue | Mandatory for QFZP | Per authority rules |

| Mainland Market Access | Unrestricted | Limited (tax impact) | Not permitted |

| Transfer Pricing Rules | Yes | Yes | If UAE nexus |

The 2026 Decision Matrix: Which Structure Makes Sense for Different Business Types

Before corporate tax was introduced, the choice between mainland, free zone, and offshore structures was largely driven by cost, ownership rules, and licensing flexibility. In 2026, tax positioning is often the deciding factor.

Your primary customers are within the UAE mainland.

Free zone companies that generate significant revenue from mainland clients, especially service-based businesses, struggle to meet QFZP conditions. If most of your income comes from UAE-based customers, a mainland structure is often the more stable and compliant option.

Mainland also makes sense if your taxable income is below AED 375,000. At that level, you are effectively taxed at 0%, just like a qualifying free zone company but without needing to meet strict eligibility criteria.

Additionally, mainland structures are required for certain government contracts and regulated activities, making them essential for businesses operating in those sectors.

Your revenue is primarily international or derived from other free zone entities. This is where maintaining QFZP status becomes realistic. Businesses with minimal mainland exposure are better positioned to meet the qualifying income and de minimis conditions.

Free zones are particularly effective when:

- Taxable income is significantly above AED 375,000

- The business has real substance (employees, assets, operations) within the free zone

- Activities fall within qualifying sectors as defined by the Ministry of Finance

However, this structure only works if all conditions are consistently met. The margin for error is narrow.

Your activities are primarily outside the UAE. Offshore entities are best suited for:

- Holding international investments or assets

- Structuring family wealth or succession planning

- Conducting business with no UAE operational footprint

If there is no UAE-sourced income or permanent establishment, the entity may remain outside the UAE corporate tax system. However, any level of UAE activity, direct or indirect, requires careful legal and tax analysis.

The most expensive mistake in 2026 is operating as a free zone company under the assumption that you qualify as a QFZP when you do not.

Businesses at high risk include those with:

- Significant mainland client revenue

- Weak economic substance

- Failure to meet the 5% de minimis threshold

The consequences are immediate:

- Application of 9% corporate tax

- Loss of QFZP status for five consecutive tax periods

Bottom Line

The mainland vs free zone vs offshore decision is no longer a simple structural choice. It is a tax, compliance, and operational strategy decision.

What worked before 2023 may not be the most efficient or compliant structure in 2026.

Businesses that take the time to reassess their setup now can avoid unnecessary tax exposure, reduce compliance risk, and operate with greater clarity going forward.

Is Your Current Structure Still Optimal?

If you are unsure whether your current structure is still optimal, or if you want to confirm your QFZP eligibility before your next filing, Protax can help. We provide detailed structural tax reviews to give you a clear, accurate picture of where you stand and what to do next.